The resurging malaise around PPPs

It is difficult to imagine a more momentous time to write this commentary on the case for sustainable infrastructure and sustainable public private partnerships (PPPs).

At the baseline, financial market volatility might again be with us. In the wake of a rise in interest rates in the United States, stock markets around the world experienced a turbulent correction in early February 2018. The S&P 500 Index and the Dow Jones Industrial average fell by over 500 basis points, and indices all over the world followed similar patterns. Since then, seven weeks down the line, markets have remained skittish. Volatile markets spark a renewed interest in infrastructure, which offers long-term investments for the patient. They help shield investors from market turbulence, provide an option for diversifying portfolios and, if interest rates rise, enable investors to pick up well-rated infrastructure bonds that may be trading at a discount. The caveat in this in picture, however, is the resurging malaise around public–private partnerships (PPP).

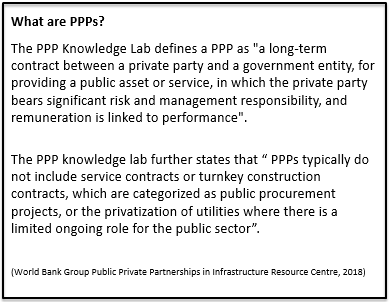

PPPs are vehicles for blending public and private capital and expertise to deliver public infrastructure and public services. Experimentation with PPPs began centuries ago, but its recent history is littered with controversies about projects that are believed to have cost taxpayers much more than if the public sector had delivered the same asset or services itself. In developing countries, more fundamental problems arise when poorly planned PPP have rendered essential sources, such as water, “too expensive” to be supplied to lower-income households.

When examining the renewed public backlash against PPPs, the fall of UK-based construction and integrated support services giant, Carillion, is a case in point. Carillion was one of the largest service providers to the government of the United Kingdom. It held PPP contracts with the ministries of education, justice, defence and transport. Its services ranged from providing school meals to maintaining prisons and rail networks to managing motorway traffic-control systems. It employed over 43,000 people around the world with subsidiaries in Canada, the Middle East and the Caribbean. In 2016, Carillion reported sales of GBP 5.2bn and until July 2017 recorded a market capitalization of almost GBP 1 billion. What went wrong?

At the heart of the trouble were three large PPP projects, the GBP 350m Midland Metropolitan Hospital, the GBP 335m Royal Liverpool Hospital and GBP 745m Aberdeen bypass which all experienced a complex mix of delays and cost overruns. As all these PPPs were negotiated off public balance sheets, Carillion was bearing a great deal of the financing, design and construction risks. In July 2017, the company issued its first profit warning, which saw its share price plummet 60 per cent. The key lenders—Santander UK, HSBC and Barclays—became very nervous. The company had to write down GBP 1 billion from the value of contracts, which made its GBP 900 million in debt and GBP 600 million in pension deficits much harder to manage. In January 2018, Carillion went into liquidation, leaving a large cross-section of public services scrambling to find both the budgets and alternative solutions to keep operations afloat.

A part of the Carillion failure is certainly down to poor governance; the company had become both too large and too diversified for management structures to keep pace. It is also important to note that the public sector is at fault. In the quest to keep debt off public balance sheets, Carillion was awarded two major public contracts after its profit warning of July 10, 2017: on July 17 Carillion was awarded a GBP 1.4 billion contract with High Speed 2 Ltd and in November 2017, was awarded the GBP 130 million London-Corby rail electrification contract. And if the Carillon downfall was not bad enough, in late February 2018, Capita, another UK-based business service provider holding large contracts with the UK government, was reported to be in financial stress. Capital provides services to Transport for London, the National Health Service, the UK Armed Forces and runs the UK Teachers Pensions Scheme.

On the other side of the Atlantic, President Trump’s USD 200 billion plan on “Rebuilding Infrastructure” provides those of us that want sustainable PPP with added cause for concern. The proposed USD 200 billion is positioned to be used to crowd-in USD 1.5 trillion from private investors, states and municipalities. While this, in itself, is quite problematic (in light of ever-increasing sovereign borrowing by the United States), the White House “Legislative Outline for Rebuilding Infrastructure,” which presents the eligibility and selection criteria for this plan, presents particular concern. The criteria with the highest ranking, that of 70 per cent, is the potential for the project to secure funding from non-federal sources. The potential of the project to “spur economic and social returns on investment” is ranked far below, at 5 per cent. Such criteria are likely to favour trophy projects and opulent developments, which have strong revenue streams and attractive financial returns. Essential infrastructure that keep lower-income citizens in work and school may well be overlooked.

Where PPPs begin to disappoint

As proponents of sustainable infrastructure, we believe that it is important to recognize that PPPs present both risks and opportunities. Because bad news travels faster than good news, we are all aware that PPPs are massively complex, expensive to plan and prepare, and extremely difficult to negotiate. It also does appear that despite the use of the most sophisticated public sector comparators (PSC), PPPs do not always deliver value for money for taxpayers. (PSC is a methodology used to estimate the cost that the government would pay if it were to deliver an infrastructure project by itself. PSC is, therefore, the key tool in determining if a PPP arrangement is likely to be cheaper and bring better value for money than if the government were to deliver the asset by working alone).

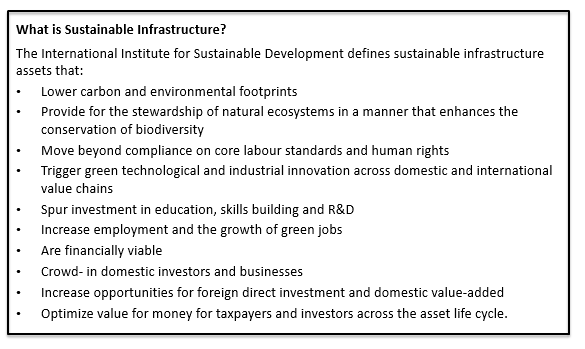

If we are to realize the UN Sustainable Development Goals, public assets and services have to be designed, built, financed and operated with sustainability in mind. In tandem, the development of sustainable infrastructure has the potential to trigger the deployment of clean technologies and the “greening” of value chains in an unprecedented manner. Given that governments are spending over 15 per cent of GDP building and upgrading public assets and services, and that 80 per cent of the infrastructure stock in middle and lower-income countries is yet to be built, is it a missed opportunity to not direct this large spending at building circular economies and valuing natural and human capital? In order to do this, governments need to work in better partnership with the private sector. By concluding that PPPs are perpetually failing, are we not hastily throwing away the baby with the bathwater?

Let us remind ourselves of the realities around PPPs:

- PPPs are tools, and like all tools, we can use them well or not so well.

- The deployment of public infrastructure is a public mandate. Governments are in the driver’s seat, and therefore the onus is on them to plan, prepare, procure and financially structure PPPs in a manner that is cost effective for themselves.

- Private counterparties seek efficiencies that will increase financial returns. This will not be any different in the case of PPPs.

- Planning and negotiation PPPs requires collaboration across a range of skills and disciplines. It also requires reliable information on demand, revenues, capital and operating costs and ever-changing parameters, specifically those to come in the next 10 to 20 years. Because PPPs are negotiated as long-term contracts, forecasts on variables such as demand, revenue and the cost of financing are important to determine which risks are best borne by the public counterparty and which can be passed on to the private sector. Governments should also be able to interpret these forecasts and use them to negotiate on the allocation of risks. Bear in mind that while such skills are rare in lower-income countries, they are also hard to find in even the most developed.

- Following on from the above, governments need to be realistic about the expertise and capacity of the private sector. This is particularly important in middle- and lower-income countries, where the private sector might be weak, but will take on the performance risk anyway, as it is “too big of a deal to turn down.” In these instances, both counterparties need to be wise and walk away when conditions for partnership are not right.

- In the case of PPPs that seek the participation of private capital holders, it is very important to ascertain if private capital can bring advantages that cannot be delivered by public financing. In industrialized countries, governments are likely to be able to borrow at a lower cost than private capital providers. In middle- and lower-income countries, borrowing at any cost can be difficult due to structural adjustment commitments and caps on public borrowing.

The International Monetary Fund (IMF) is concerned that many developing countries have unsustainable levels of borrowing; 14 African countries are deemed to be in “debt distress” or at high risk of it. In February and March 2018, Kenya and Senegal issued bonds to the value of USD 2 billion and USD 2.2 billion respectively. Angola, Ivory Coast and Ghana have announced that they plan to do the same in the coming weeks. These debt issuances are earmarked to fund infrastructure, and investors in search for higher yields were quick to respond. (The bond issue from Kenya was seven times oversubscribed even through its sovereign credit risk rating was downgraded a week before the issuance). The rush in the issuances of African bonds is no doubt due to the expected rise in interest rates in industrialized countries. The problem, however, is that the median debt level across middle-income African countries is above 50 per cent of GDP. As interest rates rise in North America and the EU, African governments will have to spend more to service these bonds at commercial rates and this will strain cash-strapped public budgets even further.

- The crux of the issue is that governments look at PPPs as means to keep debt off public sector balance sheets. The 2016 Eurostat Guide to the Statistical Treatment of PPPs (EPEC, 2016) states “an excessive focus on off-government balance sheet recording can be at the expense of sound project preparation and value for money and may push public authorities to use PPPs where not appropriate.” This is the worst position from which to plan PPPs, because unless both counterparties have “skin in the game” the partnership will fail. If the public sector does not carry the project on its balance sheet, the responsibility for ensuring its success and the incentive for optimizing value for money can be greatly eroded. The private counterparty in return looks for every opportunity to cut corners, reduce costs and maximize returns. From their perspective, it is the principle of risk and return. If they carry a greater burden of the risk, they seek to be rewarded with greater returns.

- Risk allocation, the cornerstone of PPP, is also very project-specific. Is the private sector better at designing and building assets, and can it do it more cost effectively than the public sector? Do PPPs work best when there are stable and steady returns from fees, charges, bills, tolls and the like with no enhancement from public subsidies? Can the private sector take on environmental and social risks when public due diligence is poor? The answers are not easy, for it all depends.

- PPPs bring up a very difficult debate on how comfortable citizens are when private enterprises are involved in the delivery of fundamental services. These perspectives are not always consistent across countries. In the United Kingdom, for example, citizens accept that private enterprises deliver water but are opposed to toll roads. In India and Australia, it is the exact opposite. In France, affermage contracts (the French PPP lease contracts) are used to deliver water, treat effluents and finance, build and maintain highways, but service contracting in public transport and education remains a heated political debate.

- PPPs are also targets for “political capture.” Politicians favour PPP projects because they provide for good public relations. Building infrastructure demonstrates an active government—taxpayers witness the ongoing construction, take pleasure in complaining about construction-related inconveniences and look forward to better services in the immediate term. On the downside, infrastructure projects take a long time to plan, and in the rush to launch due diligence and negotiations, environmental stewardship, and social and economic value-addition are often overlooked. The focus is very much on “getting the deal done” rather than on ‘”if the project is planned to trigger sustainable development.”

Designing more sustainable PPPs

Despite these challenges, the quest to realize more sustainable and equitable PPP partnerships that bring value for money for both counterparties is one worth pursuing. In many ways, this is a prerequisite if we are to position sustainable infrastructure as a driver of sustainable development.

The best place to start might be to help the public sector become more astute negotiators and customers.

For example, let us begin with the fundamentals of master planning. Instead of planning infrastructure projects as discrete entities (and planning one project here and another there), time and project preparation costs can be optimized if projects are planned in clusters and, from there on, as a system. This will also ensure that environmental, social and economic gains at one end of the system are not causing negative impacts in another area. Policies and implementation efforts directed at infrastructure project pipelines, project preparation funds and PPP units should all prioritize systemic planning. Moreover, systemic planning can possibly be facilitated by regulatory technology or “reg tech,” i.e., the use of financial technologies to increase the efficiency of regulation and supervision.

We also need to help policy-makers build skills on the understanding and pricing of risk. This takes us to the fundamentals of project finance. To deploy sustainable infrastructure, public investment decisions should not be based only on cost–benefit analyses but also on whether the project brings acceptable returns and can meet debt service obligations across its life cycle. Policy-makers therefore need to be able to use project finance analyses in addition to the traditional cost–benefit analyses on which infrastructure spending decisions are made.

We also need a policy mindset that moves away from focusing on the lowest bidding price. It is here that we come to expertise on sustainable and smart public procurement. Procurers and PPP planners are often petrified to select alternatives with more value across the asset lifecycle for fear of being reprimanded for not choosing the cheapest option on offer. Alternative strategies include the most economically advantageous tender as mandated by the EU Public Procurement Directive, 2014. Similarly, policy-makers in India debate on the merits of selecting the mean price quoted across short listed suppliers. In the United States, infrastructure investors promote the Guaranteed Maximum Price contracting approach, under which the counterparties agree that the contract sum will not exceed a specified maximum. To facilitate the implementation of these strategies, we can continue to explore the use of blockchain-based smart contracting technologies. They provide for more transparent price discovery and are being used by many cities—including Dubai, Geneva, Moscow, Helsinki and Tallinn, for example—to deploy a range of public services.

Contracts and concession agreements also need to be specific about the environmental, social, economic and financial performance expected from both counterparties. This then provides the incentive for governments, investors and project developers to work together to determine who is best positioned to take on different risks, thereby increasing the potential of the PPP to delivery value for all. The 2017 edition of the World Bank Group's Guidance on PPP Contractual Provisions is of particular concern. This guidance was issued after many years of debate on the value of standardizing PPP tools to increase certainty and predictability in infrastructure investment in lower-income countries. It includes sample contract language and commentaries on legal options that governments may adopt in the drafting of their national PPP laws and contracts. As pointed out by several stakeholders, including IISD, these guidelines are skewed toward the interests of private counterparties and, hence, do not provide the basis for realistic and equitable risk allocation between public and private counterparties. PPPs that are negotiated on biased and inaccurate fundamentals will most certainly fail or—in the best of cases—not take off at all.

Reading through the arguments made in this commentary, stakeholders will question if the above suggestions are indeed practical. Government jobs attract policy mindsets that are cautious and risk averse. Negotiating PPPs may require a more entrepreneurial temperament that will seek to align both public and private interests and optimize value for money across the asset life cycle. In addition, entrepreneurial policy-makers need bolder bosses who will stay true to sensible plans and projects irrespective of election cycles.

The real questions that taxpayers face in the PPP debate are perhaps more fundamental.

Are we comfortable with the private sector sharing the risks and responsibilities in the delivery of public assets and services? And are we comfortable with the private sector earning profits as it delivers on these risks and responsibilities?

Can the public sector bring us better value for money if it works alone to finance, design, build and operate public assets? And will we be more accommodating if public sector investors, operators and suppliers fail to deliver as tasked?

Regardless of what our individual responses may be, we cannot avoid circling back to our point of departure; if we want sustainable infrastructure to lead the way in achieving the UN Sustainable Development Goals, PPPs need to be planned in order to ensure better value for money for all.

References

Brauch M. D. (2017, December). Contracts for sustainable infrastructure: Ensuring the economic, social and environmental co-benefits of infrastructure investment projects. IISD. Retrieved from https://www.iisd.org/sites/default/files/publications/contracts-sustainable-infrastructure.pdf

Chao J. (2016, December). How are PPPs really financed? World Bank Blogs. Retrieved from http://blogs.worldbank.org/ppps/how-are-ppps-really-financed

Cohen, P., & Rappeport,A. (2018, February 12). Trump’s infrastructure plan puts burden on state and private money. The New York Times. Retrieved from https://www.nytimes.com/2018/02/12/business/trump-infrastructure-proposal.html?emc=edit_th_180213&nl=todaysheadlines&nlid=72458080

The Economist. (2018, March 8). African countries are borrowing too much. Retrieved from https://www.economist.com/news/leaders/21738366-dangers-reckless-lending-and-feckless-borrowing-african-countries-are-borrowing-too-much

The Economist Expresso. (2018, March). On borrowed time: African debt. Retrieved from https://espresso.economist.com/c3f7a5ca6fa6409448a99f5a772828a8

Egan, M. (2018, February 28). February was an insane month for the stock market. CNN.com. Retrieved from http://money.cnn.com/2018/02/28/investing/stock-market-february-dow-jones/index.html

European Investment Bank and the European PPP Expertise Centre (EPEC). (2016, September). A guide to the statistical treatment of PPPs. Retrieved from http://www.eib.org/attachments/thematic/epec_eurostat_statistical_guide_en.pdf

The Financial Times. (2018, February 6). US stocks suffer worst fall in 6 years. Retrieved from https://www.ft.com/content/af1f8e4a-0a23-11e8-8eb7-42f857ea9f09

The Guardian. (2018, February 1). UK officials met Capita bosses to discuss its financial problems. Retrieved from https://www.theguardian.com/business/2018/feb/01/uk-officials-capita-discuss-financial-problems

White House. (2018, February). Legislative outline for rebuilding infrastructure in America. Retrieved from https://www.whitehouse.gov/wp-content/uploads/2018/02/INFRASTRUCTURE-211.pdf

World Bank Group. (2017). 2016 Private Participation in Infrastructure (PPI) Annual Update. Retrieved from http://ppi.worldbank.org/~/media/GIAWB/PPI/Documents/Global-Notes/2016-PPI-Update.pdf