Public-Private Partnerships (PPP) in transport infrastructure can offer significant efficiency gains compared to public procurement options—in the right circumstances. The gains accrue from allocating to the private sector those risks they are better able to handle than the public sector, such as those associated with construction costs.

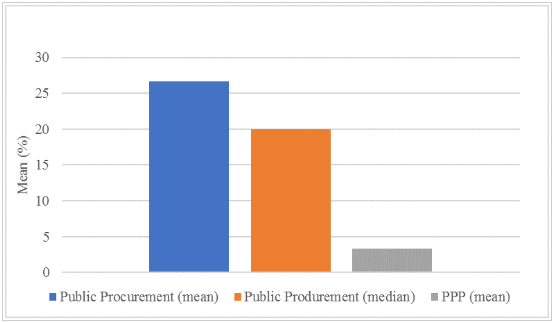

Data backs this up: findings in Construction Risk in Infrastructure Project Finance from EDHEC show that for a large number of transport infrastructure PPP projects, (including roads), construction overruns are significantly lower at 3.3 percent on average compared to public procurement projects, with a 26.7 percent overrun average.

Figure 1: Cost overruns in Transport Infrastructure Projects (%)

Source: Construction Risk in Infrastructure Project Finance, EDHEC, Blanc-Brude & Makovsek, 2013.

This means that on average efficiency gains from overruns between public procurement and PPPs are around 23.3 percent (see Figure 1). However, to evaluate whether PPPs make sense in any particular instance, these gains need to be traded-off against the incremental costs of the PPP approach. Besides some basic prerequisites related to institutions and capacity to prepare and manage PPPs, the country risk rating is a critical parameter. Unless the country has a minimum risk rating of at least BBB, costs of financing can be higher than the potential gains. Even a glance at global country risk ratings clearly indicates that the financing costs limit the utility of traditional PPPs in many of our client countries.

How then can these countries benefit from potential efficiencies and financial flows that private participation can bring to infrastructure? Indeed, there is often a chicken and egg problem—country risk ratings depend in part on the institutional environment, and the political commitment needed to create a market-friendly institutional environment requires some “good” experience with private participation.

One possibility to introduce cost-effective private participation could be lengthening the term for performance-based contracts in the road sector. For the last two decades, many developing countries have started implementing and financing performance-based road rehabilitation and maintenance contracts (PBC or CREMA), often a 5-10-year contract, where payments funded by public sources and multilateral loans are made on the basis of the quality of the asset provided (an example here would be having the road within a specific roughness limit). The contractor takes the risk on the resources, quality, and quantity of work.

PBC contracts have built important experience and skills in low-income countries. For countries with this experience, a variant of the PBC—lengthening the term to 12–15 years, reinforced by innovative financing tools, offers the potential to explore PPPs in a cost-effective manner.

The PBC presents the private sector and government a well-understood contract and operating environment as well as a clear set of rules and practices.

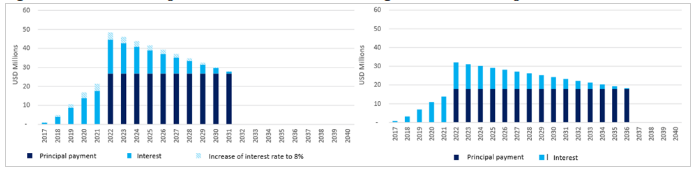

Importantly, the World Bank Group offers project-based guarantees that can guarantee a portion of the debt to reduce the financing risk and its costs. This means that lenders may be more willing to provide longer-term financing and the amount of debt service could be lower. An example of the impact of a guarantee on 50 percent of the total debt of a $383 million investment, with a four-year construction period and 30:70 equity to debt ratio in a Latin American country rated at BB without long-term financing, shows that a one percent interest rate reduction and a five-year tenor extension will have significant impact on debt service and cost of the project (see Figures 2a and 2b). This financial instrument will help governments secure efficiency gains from PPPs and bring in the private sector to finance infrastructure and service provision.

Guarantee impact on interest and tenor

Figure 2a. Without IBRD guarantee Figure 2b. With IBRD guarantee

The World Bank’s Transport and Digital Development Global Practice is working with Liberia and Bolivia to introduce such project-based guarantees to upgrade PBCs in the road sector to essentially short-term PPPs with private sector financing. In these countries, PPPs in the road sector need a modular approach to attract international investors by upgrading PBC to PPP contracts through guarantees, creating long-term financing for PPPs, and knowledge to address more complex projects.

PPPs in low-income countries or in countries with weak institutions will need not only to strengthen their institutional arrangements and capacity to prepare projects and manage PPP contracts, and at the same time show results (efficiency gains) in terms of cost/km between PBC (funded by government and multilaterals) and short-term PPPs with private financing.

This blog was originally published on the World Bank Infrastructure & Public-Private Partnership Blog on 26 June 2018.